Hyatt hotel founder Jay Pritzker amassed a $15-billion fortune through his hotel business in 1957. He died in 1999, and his heirs, the Pritzker family, were to continue the Hyatt chain's empire as a family-run corporation when he passed away that year. Soon enough, two of Jay Pritzker's grandkids, Matthew and Liesel Pritzker, launched a lawsuit against their father, Robert Pritzker, and their other relatives in 2002.

They alleged that almost $1 billion had been wrongfully withdrawn from their trust funds. When the case was resolved in 2005, Matthew and Liesel both received $500 million. All claims on additional family assets were waived as a result of the lawsuit's settlement, while the other 11 people split the rest of the family's assets among themselves.

There have been many horrifying probate proceedings, and this is only one of the most well-known ones. As they say, people who don't learn from other's mistakes are doomed to repeat them.

What Is Probate?

Probate is the legal process of reviewing a will to determine if it's authentic and legitimate. Probate is also used to describe the general administration of a person's estate who died without a will.

When an asset holder dies, the court chooses either an administrator (if no will exists) or a specified executor in the will to oversee the probate procedure. This entails gathering the assets of a dead individual to satisfy any obligations lingering on the person's estate and distributing the estate's assets to beneficiaries.

When Is Probate Necessary?

Generally, your spouse is the first person to receive a portion of your estate. You may be required to go through the probate procedure if you aren't married and your assets transfer to other family members in a certain sequence, usually beginning with the surviving children and then other relatives depending on their proximity to you.

The following situations can also qualify you to undergo this process.

1. There's No Will and Testament

When a decedent dies without a valid last will and testament and the assets of the deceased fall into one or more of the categories listed below, the assets must often be probated before they may be transferred to the decedent's legal heirs.

2. No Designated Beneficiaries or They Predeceased the Decedent

In most cases, the deceased's assets must be probated to be distributed to the named beneficiaries of any of the following: a medical or health savings, a retirement account (like a 401(k) or an IRA), an annuity, or a life insurance policy. If the deceased didn't name any beneficiaries at all, or the named beneficiaries of any of these assets died before the deceased, then the assets must be probated.

3. The Assets Are Solely Under the Deceased’s Name

Property that's solely held by one person and has no other owners or a payable on death (POD) designation must be probated, especially if the decedent's beneficiaries aren't named as co-beneficiaries or co-owners.

Keep in mind that numerous states have made an exception for motor vehicles. Let's take a look at Florida and Tennessee, where a deceased person's heirs at law might get a motor vehicle without having to create a probate estate.

Additionally, some states provide a simplified procedure for "small estates" that takes far less time than a complete probate procedure. In the state of Florida, a small estate is defined as one that is worth less than $75,000 in total.

4. It’s a Tenant-in-Common Asset

If the deceased possessed property as a tenant in common with others, the decedent's tenant-in-common share will almost always need to be probated in order to transfer ownership from the decedent's name to the heirs.

Note that a tenant-in-common interest that has been transferred into a revocable living trust prior to the decedent's death doesn't need to be probated.

If you pass away without a will, what happens to your assets depends on your state's laws. For instance, community property rules apply to your estate if you live in Nevada, Arizona, New Mexico, California, Texas, Idaho, Wisconsin, Louisiana, Nevada, and Washington.

According to community property laws, both spouses hold equal shares of marital property. Assuming that you got married and bore no children when you died, the court will distribute the assets to your spouse. In other cases, probate courts will use state inheritance regulations to decide how your wealth will be allocated.

What Has to Go Through Probate Court?

Probate court will handle everything when the deceased possesses no will. Whatever their estate planning indicates, the following will always happen.

Partner-owned investment properties: A probate court will intervene for the property that's titled as "tenants in common" and without specific instructions in a will on how the share would be distributed.

Sole ownership properties: Property that's only titled in your name will be subjected to probate to identify ownership. You may circumvent this in certain states by adding "TOD" (transfer on death) or "POD" (payable on death) to the deed or title.

The inheritance where the heir predeceases the giver: Unless you amend your will, a listed beneficiary that dies before you will call in the courts to settle this portion of your assets.

Non-titled property: Basically, whatever you possess that isn't documented is considered "non-titled." Furniture, clothes, and household appliances might all come under this umbrella term. By specifying these goods and clearly expressing your desires, you can eliminate the need for probate.

What Does Not Have to Go Through Probate Court

Some property and assets won't have to go through the probate process if the following situations apply to your case.

There's an indicated beneficiary: Take a life insurance plan as an example. By naming a beneficiary on an asset, the death benefit flows straight to them without going through probate.

Properties that are under joint titles: Alternatives to probate include community property with right of survivorship, tenancy by the entirety, and joint tenancy with right of survivorship. Jointly owned residences, bank accounts, stocks, and automobiles go to the joint survivor. Don't forget that when you title a property jointly, you give up half of it.

Living trust items: The property under inter vivos trusts or revocable living trusts isn't probated, so it goes immediately to the heirs. Simply form a trust and transfer the property ownership to it. Many individuals designate themselves as trustees to preserve complete control of the trust assets after death without the waiting period.

Transfer on death (TOD) assets: Accounts known as "transfer on death" enable you to choose one or more beneficiaries to skip the probate procedure when you die. There are no complicated steps involved in setting up an estate plan, and beneficiaries can quickly collect their share of the assets once the owner passes away.

What Is the Probate Process?

Whether you have a will affects the outcome of the probate procedure in court. The main distinction is that without a will, the court will appoint a Personal Representative to handle your estate distribution. In the absence of a will, only the start of probate differs while the rest remains the same.

BurialLink Quick Guide to the Probate Process (1)

BurialLink Quick Guide to the Probate Process (2)

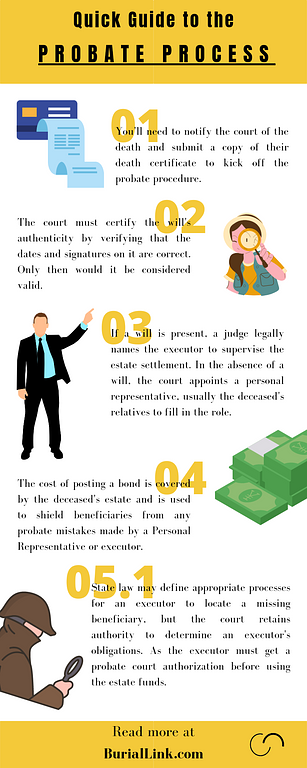

1. Death Certificate

The quickest approach to get certified copies of the death certificate is to request them from the funeral director handling the cremation or burial arrangements. The cost of this service is commonly included in the bill by funeral homes.

It's a good idea for many to pick up a dozen extra copies from the morgue. If you want more copies in the future, you must make official written requests to the state department or county in charge of vital data.

In most states, only the estate's executor, close relatives, or someone inheriting from the dead have the right to acquire certified death certificates. So, if you shop online, you'll have to provide a picture ID (or a duplicate if you order in person).

2. Have the Will Validated

Most state laws require an executor to submit a will with the local probate court soon after the death of the deceased. Then, a probate court judge examines whether the will is legitimate.

This normally entails a hearing in which all of the will's specified beneficiaries have a right to look at the document and oppose or accept their position in it. The court determines how to proceed in instances where wills are challenged.

Self-proving affidavits can be used to assist, construct, and complete wills in various situations. These will be signed by the grantor and witnesses. Generally, these papers are sufficient for the court to initiate the probate procedure.

3. Select Someone to Conduct Probate

An executor is a person who is either specified in the will or appointed by the court. They're legally obligated to ensure that the stipulations of a will are fulfilled and the affairs of the dead are completed.

Although state laws differ, it's typically prohibited to select an executor who is a convicted felon or a minor. Other jurisdictions require out-of-state executors to also be the estate's principal beneficiaries.

The executor will be issued Letters of Testamentary after taking an oath and swearing in. Third parties, including investment and banking institutions, are made aware of their legal capacity to operate for the estate through this document.

4. Post a Bond

A probate bond is a court bond issued on behalf of an executor of a deceased's estate. It ensures that the estate's executor will follow state laws and the conditions of the decedent's will or trust.

Should the executor violate either the conditions of the trust/will or the state laws, heirs, family members, and other stakeholders can file a claim against the bond. It's then the surety who sold the probate court bond who will compensate the plaintiff.

Remember that there's no legal need for an estate executor or administrator to be bonded. In fact, it's possible for the heirs to waive it, assuming that the deceased's debt was a small amount.

5. Inform Beneficiaries & Creditors

An executor must identify all heirs and beneficiaries at the start of the probate procedure. When a beneficiary or an heir is absent, the executor must make reasonable efforts to identify and contact them. For instance, a court might order an executor to publish a probate case notice in a local newspaper.

They'll also be required to contact other known partners, relatives, or friends, search online (including social media), check last known residences, hire a private investigator, check property records, or contact prior employers.

Note: An executor must file an affidavit with the court explaining their attempts to locate a missing heir. In their absence, the probate court may be asked to extend or end proceedings. A few states also allow the missing beneficiary's share to be distributed by law or even by will.

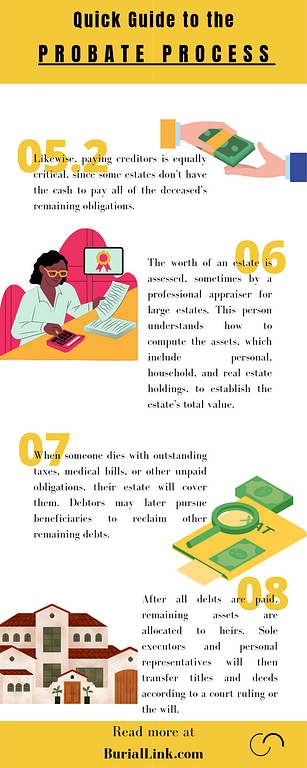

A notice to creditors and debtors will also be published in the legal organ when the probate is opened, which will run for four weeks. This notice informs anybody who has a claim against the deceased or the estate to come forward and notify the court.

After the publication ends, creditors have three months to file claims before the administrator or executor can start paying safe distributions. Payments to beneficiaries or heirs can only be made if the estate has adequate cash to satisfy all known creditors (including taxes).

6. Determine Value of Assets/Property

You will need to know the property worth for tax, probate, and final distribution considerations. To get an estimated value, you can either pay an independent specialized valuer or receive three free evaluations from three separate real estate agents.

When the property is sold, the final sales price will decide the portion of money that will contribute to the overall estate value. As an executor, you should get a professional evaluation if the property's value is likely to be a point of contention among the beneficiaries.

7. Pay All Fees and Debts of the Deceased

Many of the expenses will need to be paid immediately, without waiting for the executor to form an estate bank account and write checks. In most cases, the heirs should pay the current expenses.

If these costs aren't covered, valuable items may be lost or ruined. However, if the beneficiaries have previously agreed not to retain particular property, like a property worth less than the mortgage, then they could stop paying its mortgage.

A bankrupt estate looks to have more obligations than assets. Pay no debts you don't have to, since state law will create a priority list for you to settle. Once you pay low-priority debtors, you'll be liable for the amount paid.

8. Distribute Remaining Assets

After gathering all assets, paying creditors, and filing taxes, the executor or administrator can start the distributions. The executor should make specific gifts first, then distribute the residuary estate, which includes all residual assets. If there's no leftover after making all the specific gifts, the residual beneficiaries get nothing.

Personal property would be divided pursuant to the will or to the heirs in an intestate estate. In case the beneficiaries don't want some or all of their personal property, it should be sold or given.

Sometimes an estate sale is required to clean out the deceased's house of unwanted personal possessions. Items such as rare artwork, yachts, antiques, aircraft, or other valuables can be auctioned, as well as undesignated properties.

Stocks and investments might be liquidated or immediately handed to the heir. In the era of cryptocurrency and technology, digital assets can have unique values and distribution issues. To value and transfer the estate's distinctive assets, extra specialized bodies will be called to weigh in the situation.

How to Avoid Probate

Probate without a will can take a long time (even years). While costs vary per state, probate often entails extra expenses. Finally, one of the main reasons individuals avoid it is for privacy.

Probate is a stressful process, but there are a number of methods to avoid the burden.

Establish a Living Trust

A living trust is legal paperwork that specifies where your assets will go when you die. A third party, or "trustee," will hold and manage your assets under a living trust. These assets might include real estate properties, vehicles, bank accounts, or other significant personal items. Following your death, the trustee will be able to quickly transfer the trust assets to their specified beneficiaries, allowing an end-run around probate.

Give Away Assets (While Still Alive)

Giving gifts prevents probate since you no longer own the property after you die. Between 2020 and 2021, you may donate up to $15,000 per person annually without incurring a gift tax. Giving before you die reduces your probate expenses as the assets' current value increases the charges you'll incur in the process.

Small Estate

Regardless of probate assets, if the court deems the decedent's property a small estate, it will avoid the whole probate procedure. Of course, the state may define this term differently. For example, in New York, small estates are defined as being under $50,000, while California recognizes them as $166,250 or less.

Even if the estate fulfills the criteria, it may be subject to further limitations. Among other things, in New York, an estate can only include personal property. Proprietary property is subject to probate unless it is kept under a joint tenancy.

Once the estate fits these conditions, the personal representative or executor will complete a simplified probate procedure or sign a small estate affidavit (SEA) that the new owner will present to the entity that has possession of the asset to start the transfer of ownership process.

Title Accounts POD or TOD

Many assets can be designated for Transfer on Death (TOD). This eliminates the need for probate and permits beneficiaries to acquire assets promptly upon death. There are TOD deeds for anything from cars to real estate and financial portfolios. People like this choice since it's easier to create than trusts or wills and requires less paperwork.

The TOD deeds also identify who the beneficiaries are and what proportion of the assets they would get. Remember that if you reside in Ohio, Ohio Statute 5302.22 prohibits beneficiaries from controlling or owning assets while the individual is alive.

Pay on Death (POD) provisions, sometimes known as Totten trusts, are similar to TOD provisions. These function in the same manner, but can only be used on bank accounts rather than a variety of assets. A POD agreement is made between a bank or credit union and an account holder.

The money in the accounts will be inherited directly by the persons named in the deed. POD provisions, like TOD documents, deny beneficiaries access to bank accounts until the account holder's death is confirmed.

Title Property Jointly

An important property law concept known as co-tenancy describes how two or more persons may share ownership of a single piece of property. Joint Tenant With Right of Survival (JTWROS) is a kind of co-tenancy that provides equal rights to the asset, as well as the right of survivorship for all co-owners. As a result, the asset is open for usage by any party. Upon the death of a tenant, the remaining tenant(s) receives their share.

It's often used between married couples or parents and their children. It may, however, be established even if the parties aren't related. Assets and bank accounts that might be included in this form of legal partnership include but are not limited to:

Brokerage fund accounts

Real estate assets

Mutual funds

Savings and checking accounts

If one or more of the persons involved sells their share to someone else, this agreement will be terminated. In this way, it becomes a less restricted kind of joint ownership known as a tenancy in common (TIC).

Popular Questions About Probate

Clients have the right to ask the following questions until they're certain that they've selected a suitable attorney to represent them or their estates.

How Long Does Probate Take?

Disputed wills, tax issues, and inheritance concerns all affect how long probate takes. It can even take up to two years from the decedent's death. In rare cases, the process can drag on for decades to resolve issues and address the related litigations.

How Much Does Probate Cost?

The probate procedure comes with a number of charges. And variables that might affect these fees include the estate's size, whether you have a will, and your last known residency before death.

Executor's compensation: This charge is sometimes a proportion of the estate's worth. Under the California law, executors get 4% of the first $100,000, 3% of the following $100,000, 2% of the next $800,000, and so on.

Attorney costs: Most probate lawyers bill by the hour, and their rates can range between $350 and $600 per hour. If the client owns a small estate, they can opt to charge a fixed fee, which typically starts at $3,000.

Public notice fees: The executor must publish in local newspapers to notify the deceased's creditors through a Notice to Debtors and Creditors. This typically costs $10 for 100 words plus a $5 affidavit fee, with the cost increasing depending on the length of the notice. This is paid out of the estate.

Probate bonds: It costs $150 to $1,700 to purchase a probate bond valued under $200,000. While it costs more than $1,700 to insure a bond worth over $200,000. Note that a bond's value and bondholder's creditworthiness are both factors in pricing.

Court proceeding fees: Depending on where you live, the filing costs might vary significantly. As a rough estimate, you'll spend $175 to initiate the process of probating an inter vivos trust, then expect additional costs along the way.

What Is Probate Real Estate?

Indigent (no will) deaths are decided by the state's probate laws. Although the sequence of inheritance varies by state, the surviving spouse usually inherits first, followed by the children, parents, and other relatives.

Without heirs, the property will pass to the state, and the court will have final say over the bidding and sale of these assets.

What to Bring to Your First Probate Hearing

A judge will set the first probate hearing so interested parties may object. Doing so permits the court to legally designate the person who will supervise the division of assets and other parts of the estate. Along with this, the court will provide legal documentation that'll assist a personal representative or executor to settle the estate affairs, like:

Letters of Authority

Letters of Testamentary

Letters of Administration

What Is a Probate Will?

The term "testator" refers to an individual who has left behind a will. Probate begins when a testator dies, and the will's executor is in charge of filing its petition. A financial adviser is often the executor, though it can also be named from the deceased's family.

Even if you created it yourself, a will is legitimate as long as it is signed in your own handwriting. There's no need for witnesses, but try to be as detailed as possible to avoid misunderstandings. However, hiring a lawyer can be the safest route for you, especially in handling large assets.

Do you have a plot to sell?

List your plot to find a buyer. Signing up is easy!