The Centers for Disease Control and Prevention's (CDC) 2019 federal report revealed that New York has the third-highest average life expectancy in the United States at 80.7 years.

However, they also disclosed that heart disease, cancer, and accidents are the leading causes of death in the state, making burial insurance an appealing option. This is often sold to persons with severe health issues and little financial resources to cover their funeral costs.

Whether it's called "senior life insurance" or "final expense insurance," it's dedicated to folks who want to ensure their financial affairs are in order before they die.

What Is a Death Benefit?

When the annuitant or insured dies, an annuity or a pension's death benefit is paid to the beneficiary. These are exempted from income tax, and designated recipients often receive the death benefit as a lump sum payment.

The policyholder controls how the insurer pays the death benefit. They may choose that half of the death benefit be paid immediately and the other half a year later. Moreover, some insurers provide several payment options instead of a fixed sum.

The proceeds from a death benefit might be paid in installments or used to fund a non-qualified retirement account. Unlike a life insurance policy, retirement account death benefits may be taxed.

The SECURE Act, passed by the United States Congress in 2019, changed retirement plans, notably the death benefits associated with inheriting an IRA.

It eliminated the IRA stretch provision. Previously, an IRA beneficiary could delay required minimum distributions for life. Stretching dividends provided a steady cash stream while also spreading the tax burden.

In 2020, non-spousal beneficiaries had to disperse all inherited IRA funds within 10 years after the owner's death. There are, however, certain exceptions to the new regulation, like spouses.

How Does Burial Insurance Work?

Nearly 137 million Americans had financial difficulties due to medical expenses. Significant sums of such debt accumulate in the latter years of life, especially with long-term care expenditures in addition to hospitalizations and doctor visits.

In fact, the New York Times recently reported on the Lanes case, where they had an outstanding $257,000 bill soon after their baby had passed away. While having life insurance may pay off some of these bills, it's practical to have a standard burial insurance policy in place as well.

These insurance policies are generally about $50,000 or less and solely cover funeral or burial costs. Any leftover money might be used to pay further expenditures, including medical debt or other unpaid bills left behind.

Compared to life insurance, standard burial insurance simply involves a few medical questions rather than a complete physical exam to qualify for coverage. Meanwhile, guaranteed issue life insurance is burial insurance designed for terminally ill clients who can't purchase a policy any other way.

Let's say that Benedict died suddenly. His son Russell is his beneficiary and executor, and he has Benedict's burial insurance paperwork. Russell tells the company, which issues a check for the amount and mails it to Russell. He can then put down a deposit on a casket, start planning the burial, and still have enough money to pay for Benedict's funeral service.

The downside of these easy applications is "graded death benefits." A policy's coverage value is just a portion of the premiums paid if you die within two or three years after acquiring it. Accidental deaths, such as those in airplane crashes, are generally fully covered from the start of the policy.

How Much Is Burial Insurance?

It costs between $50 and $100 a month on average for a burial insurance policy to cover $10,000. This depends on the amount of coverage you buy, health status, gender, and age.

Remember that the cost of burial insurance coverage will be determined by several factors, including the following.

Age

Almost every insurance company tailors its pricing based on an age bracket. It's an unusual practice, but some organizations like the AARP charge in this manner.

For example, at age 50, Glenn may apply for AARP's guaranteed life insurance policy, which covers members ages 50 to 80. If Glenn died of natural causes within its two-year waiting period, his beneficiary would only get 110% of the premiums paid. Still, full benefits are provided for accidental deaths without regard to health or age.

Health

Most organizations that provide funeral insurance categorize their product into three health categories. The best health rating will cost the least, while the worst will be the most expensive.

“Preferred” or "Level": These plans always refer to the health grade with the lowest risk. They typically don't have any waiting period and come with the lowest possible cost.

"Standard" or “Graded”: These words usually refer to the middle tier rating. Typically, you would have to answer yes to at least one question on an application for a carrier to offer this type of plan to you. It will cost a bit more than their best health rating. Also, it may or may not have a waiting period.

"Basic" or “Modified”: This is the riskiest health rating conceivable. An insurer would only provide this coverage if you had serious health difficulties. This plan is often the most expensive and comes with a two-year waiting period.

Keep in mind that the amount of coverage you may get from any insurance carrier is determined by your health.

Gender

Your gender is one of the most critical elements in calculating the net cost. As men typically don't live as long as women, men will always pay more for life insurance products than their counterparts.

The HALE index, developed by the World Health Organization (WHO), evaluates how long a woman or man may expect to live without a severe injury or disease. They found out that American men can expect 65 years of "full health." In comparison, American women can expect to live for about 67 years.

You're the lone exception to this rule if you reside in Montana. Insurance companies in Montana are prohibited from offering different rates to customers based on gender per their state regulations.

Smoking History

Cigarette smoking is highly addictive and has negative long-term health consequences. It also poses the biggest health risk of any tobacco product on the market. Some insurance companies even consider e-cigarette, vaping, and hookah usage to be smoking and charge smoker rates if the product includes nicotine.

As long as you haven't smoked in 12 months, you can avail the company's nonsmoker pricing that'll save you a couple of dollars.

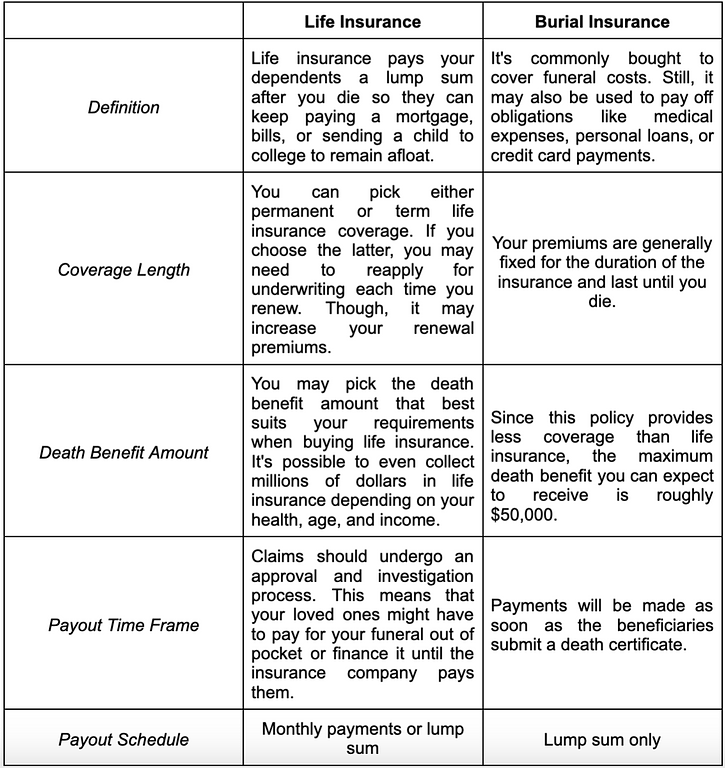

Are Life Insurance and Burial Insurance the Same?

Unlike life insurance, burial insurance doesn't require a medical assessment. After answering a few medical questions and providing your prescription history, permission is granted. Once authorized, most insurance companies can provide a policy within a few days.

Its coverage will also go toward your cemetery fees, cremation, grave monument, casket, burial plot, and other final expenses. Some policies payout within 24 hours, even without a death certificate. This is why most funeral homes take it as a one-time payment with no stipulations.

Life Insurance Versus Burial Insurance

For maximum family protection, you may wish to examine both types of coverage. Make sure this is the right policy for your beneficiaries and yourself. Remember that the surviving loved ones may greatly suffer if they don't know all of the conditions beforehand.

How Much Does an Average Funeral Cost?

As of 2019, the National Funeral Directors Association (NFDA) reported a $7,640 median cost for a funeral, including burial and viewing without a burial vault. By adding that item to the calculation, the total fees will amount to $9,135.

Meanwhile, a cremation without an urn or cremation coffin costs $5,150 on average. In most circumstances, including a cremation casket and an urn will bring the total to about $6,645.

Bear in mind that these figures don't reflect the costs associated with an obituary, flowers, markers, or monuments.

Read More: How Much Should a Headstone Actually Cost?

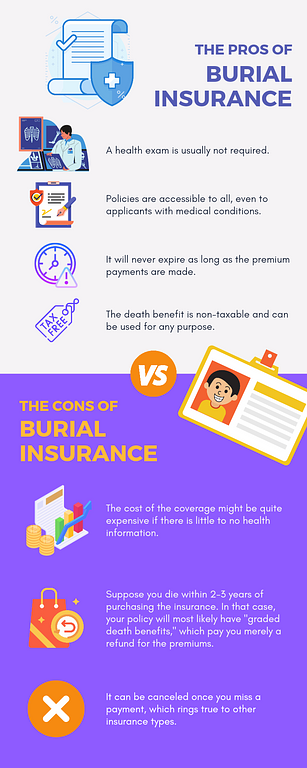

Pros & Cons of Burial Insurance

Burial insurance is an alternative if you want a life insurance policy to cover burial costs. This strategy, however, has significant drawbacks. Here are some pros and cons of burial insurance:

Pros and Cons of Burial Insurance

How Much Burial Insurance Do I Need?

Generally, the coverage you'd need depends on your preferred funeral arrangements. So, if you believe you'll be okay with minimal preparations, a $10,000 funeral insurance policy should be enough.

However, if you're set on including big-ticket items like a vault, casket, or headstone, the sweet spot may be a $25,000 insurance policy.

Did You Know? Let's say that your loved one died due to an emergency or major disaster. In that case, you might be eligible for Federal Emergency Management Agency (FEMA) Funeral Assistance that can accommodate the funeral expenses. Plus, they're also accepting applications for COVID-related deaths.

Does Social Security Help Pay for Funeral Expenses?

If the surviving spouse was living with the insured, Social Security would give them a modest $255 payment for the funeral expenses. In the absence of an eligible widower or widow, the money can be given to the deceased's unmarried or handicapped child.

When the deceased's spouse or kid has already received family benefits, Social Security will immediately release the death benefit once notified. If not, the survivor must file a claim within two years after the death.

You might need to give the deceased's death and birth certificates. You'll also be asked about the deceased's financial, familial, and Social Security status, as outlined in the SSA-8.

Do you have a plot to sell?

List your plot to find a buyer. Signing up is easy!